Copper’s Coming Chokehold

Why the World Is About to Run Out of the One Metal It Can’t Live Without

The global copper industry currently stands at a historical inflection point, transitioning from its traditional role as a cyclical indicator of industrial health into a critical strategic asset essential for the execution of the global energy transition, the proliferation of artificial intelligence, and the maintenance of national security.1 As the world moves toward 2030, the fundamental market structure of copper is increasingly defined by a persistent and widening gap between accelerating demand and a constrained, inelastic supply response.3 Industry luminaries such as Robert Friedland have argued that we are entering a “once-in-history” structural deficit, characterized by a requirement to mine as much copper in the next 18 years as humanity has produced in the last 10,000 years to sustain even modest economic growth.5

This analysis synthesizes the current supply-demand dynamics, the underlying structural drivers of consumption, and the geological and geopolitical barriers to production. It evaluates the “structural deficit” thesis by examining published forecasts from major institutional players including S&P Global, the International Energy Agency (IEA), Wood Mackenzie, and various global investment banks.

Global Market Structure: Current Supply and Demand Equilibrium

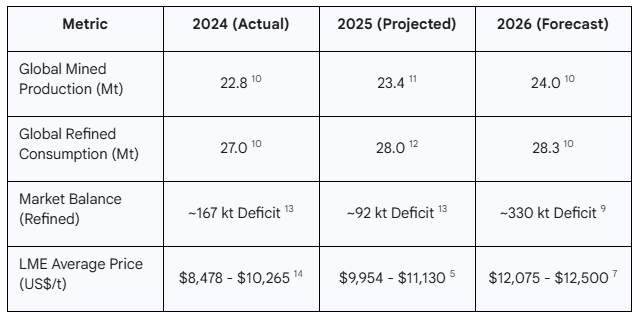

The copper market in 2024 and 2025 has been characterized by extreme volatility and record-high prices, with the London Metal Exchange (LME) cash price surpassing $13,000 per metric ton in early 2026.6 This pricing regime is not merely a short-term speculative rally but a reflection of a tightening physical market where inventories have often fallen to levels representing only 14 days of global demand.8

The 2024-2026 Market Balance

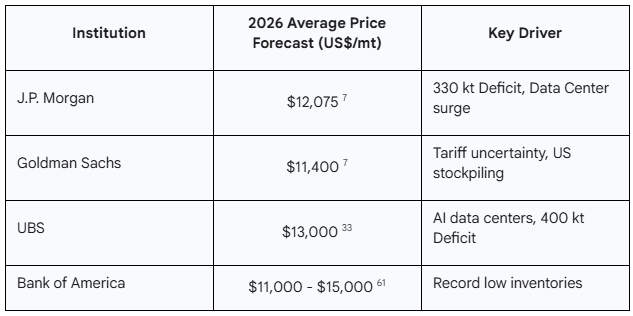

Global copper production in 2024 reached approximately 20.9 million tonnes, while demand sat at 21.9 million tonnes, creating an initial structural deficit of roughly 1 million tonnes.3 This imbalance has persisted into 2025 and is projected to intensify. J.P. Morgan Global Research forecasts a global refined copper deficit of 330,000 metric tons in 2026, even as high prices attempt to incentivize supply and temper marginal demand.9

The supply side of the market is heavily concentrated, with Chile and Peru collectively accounting for approximately 36% to 40% of global mine output.3 However, this supply is increasingly fragile due to declining ore grades, water scarcity, and political instability.18 On the demand side, China remains the dominant consumer, accounting for nearly 60% of global consumption of refined copper in 2024.10 However, the vectors of growth are shifting toward India, Southeast Asia, and Western markets driven by green infrastructure and digitalization.4

The Mechanics of Structural Tightness

The market’s structural tension is exacerbated by the “dislocation” of global inventories. While certain regions, like the United States, have front-loaded imports to build strategic reserves ahead of potential tariffs, other regions remain acutely short.9 In early 2026, U.S. copper prices traded at a significant premium to the LME due to these localized supply chain anxieties.9

Financial conditions also play a reflexive role. High copper prices and strong gold/silver by-product gains have significantly increased the margins for copper miners, with gold reaching $3,445/oz and silver $40/oz in 2025.16 While high margins theoretically encourage production, mining must compete for capital allocation against high-growth, high-return sectors like AI computing.16 Consequently, many Western miners have focused on capital discipline and mergers and acquisitions (M&A) rather than the risky, capital-intensive development of new greenfield mines.21

The Structural Deficit Thesis: Analyzing Friedland’s Predictions

Robert Friedland’s thesis posits that copper demand is “essentially infinite” because there is no rational price for a material that is absolutely mandatory for the modern world’s survival and progress.5 This “revenge of the old economy” argument highlights that while the world has focused on digital “bits,” the physical “atoms” required to power that digital reality have been neglected for two decades.5

The Quantified Gap

The gap between current production and future requirements is staggering. S&P Global analysis indicates that by 2043, humanity must match the total copper mined throughout all of history (roughly 700 million tonnes) just to sustain a modest 3.5% annual GDP growth.5 When factoring in the specific requirements of Net-Zero 2050 goals, refined copper demand is projected to double from 25 million tonnes in 2021 to nearly 50 million tonnes by 2035.24

Under the “Rocky Road Scenario”—which assumes a continuation of current trends in capacity utilization and recycling—S&P Global projects a shortfall of 9.9 million tonnes in 2035.25 This represents a 20% deficit relative to what is required to stay on track for climate targets. Even in a “High Ambition Scenario,” characterized by record-high recycling and aggressive capacity expansion, the market remains in a persistent deficit throughout the late 2020s and early 2030s.25

Strategic Mineral Security

Friedland and other analysts increasingly frame copper as a “national security issue” rather than a mere commodity.5 The transition from a fuel-intensive energy system (oil/gas) to a mineral-intensive system (copper/lithium/nickel) creates a new set of geopolitical vulnerabilities.24 Copper was added to the U.S. list of “critical minerals” in November 2025, following the European Union’s inclusion of the metal in its Critical Raw Materials list in 2023.28

The launch of “Project Vault” in the United States in early 2026—a $12 billion domestic critical minerals stockpile—underscores this shift.26 Governments are moving away from just-in-time inventory models toward building strategic reserves, which paradoxically adds further demand pressure to an already constrained market.1

Vectors of Demand Acceleration: The Four Disruptors

Wood Mackenzie and S&P Global identify four key “demand disruptors” that are fundamentally reshaping the structural requirements for copper.2 These disruptors are expected to add approximately 3 million metric tons of annual demand by 2035, while traditional uses in construction and appliances continue to grow at a baseline of roughly 2% annually.4

The Energy Transition: EVs and Renewables

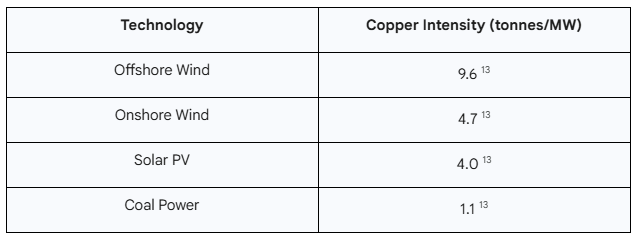

The energy transition remains the primary pillar of incremental demand growth. Solar and wind technologies are significantly more copper-intensive than traditional thermal power generation. An offshore wind farm, for instance, requires approximately 9.6 tonnes of copper per megawatt (MW) of installed capacity, compared to just 1.1 tonnes for a coal-fired plant.13

The transportation sector’s shift to electric vehicles (EVs) acts as a demand multiplier. A typical BEV contains 62-99 kg of copper, and by 2035, EV-related demand is set to double from 2025 levels, reaching an estimated 4.3 Mtpa.4 The rapid expansion of EV charging infrastructure and the necessary grid modernization to support high-voltage charging further swell the demand profile.24

Digital Infrastructure and Artificial Intelligence

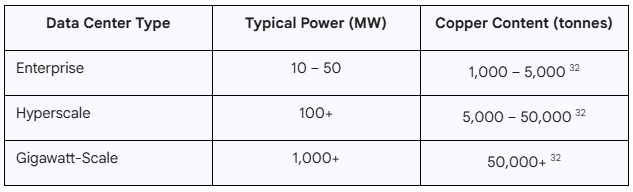

Artificial intelligence has emerged as the most unpredictable and price-inelastic demand variable.4 AI data centers operate at significantly higher power densities than conventional facilities, often exceeding 100 kilowatts per rack compared to the traditional 5-15 kilowatts.32 This necessitates advanced liquid cooling systems and massive power distribution networks, both of which are copper-intensive.32

Hyperscale AI data centers can require up to 50,000 tons of copper per facility.33 On a per-megawatt basis, contemporary data center construction requires approximately 27 to 47 tonnes of copper for wiring, cooling, and power distribution.32 For example, a single 81-megawatt installation in Chicago incorporated 2,177 tonnes of copper, aligning with these high-intensity benchmarks.32

Defense Spending and Global Security

Defense-related copper demand is inherently inelastic, as national security priorities override price considerations.30 Modern military technology—from communications and radar systems to the shells of 155-mm howitzers—depends on copper’s unique conductivity and mechanical properties.5 The recent commitment by NATO allies to increase annual defense spending to as much as 5% of GDP by 2035 is projected to add significant indirect pressure on global copper stocks as munitions and communications hardware are modernized.4

Asian Industrialization: India and Southeast Asia

India and Southeast Asia are entering a phase of rapid industrialization and urbanization that mirrors China’s historical growth trajectory but on an accelerated timeline.4 India currently accounts for only 3% of global copper demand but is expected to reach 10% by 2050.10 Combined with Southeast Asian “tigers,” this industrial surge is projected to add 3.3 Mtpa of copper demand by 2035.4 If these regions replicate even half of China’s historical urbanization patterns, their construction and power sectors alone would require an additional 5.4 Mt of copper.4

Supply-Side Rigidities: Why the Response is Lagging

The bull case for a structural deficit is as much about the failure of supply as it is about the surge in demand. The global mining industry faces a “triple threat” of declining ore grades, extreme lead times for development, and a “geographic bottleneck” for processing.3

Geological and Operational Challenges

The world is mining out its highest-quality deposits. The average grade of copper ore has declined by 40% since 1991, meaning that for every tonne of copper produced, miners must now process significantly more rock.10 This has a linear impact on the energy and water intensity of production. It now requires approximately 16 times more energy and double the water to produce a tonne of copper compared to the early 20th century.8

Furthermore, new discoveries have plummeted. Between 1990 and 2023, 239 new copper deposits were discovered, but only 14 of those were found in the last decade.10 This “discovery drought” means the pipeline of future mines is thinning precisely when the world needs it most.

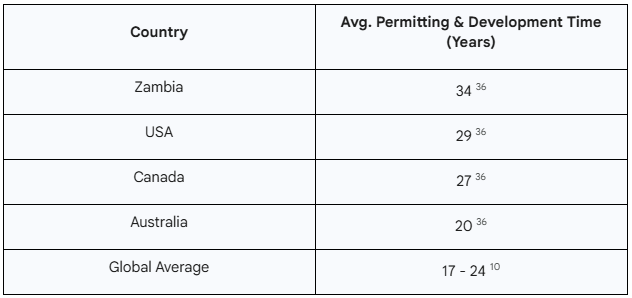

The Permitting Trap

The timeline from discovery to first production has extended to an average of 17 years globally.10 In jurisdictions like the United States, this timeline stretches to 29 years due to regulatory complexity, environmental reviews, and litigation risk.36 Even in mining-friendly jurisdictions like Canada and Australia, the process takes 27 and 20 years, respectively.36

This temporal mismatch is critical. Mines authorized in 2026 will likely not reach full production capacity until the 2040s, leaving the 2030-2035 period—the most acute deficit window—uncovered by new primary supply.1

Water Scarcity and Desalination in Chile

Chile, which produces 25% of the world’s copper, is facing a severe “mega-drought” that has drastically reduced water availability for mining operations.18 Lower ore grades require shift from oxide mining to sulfide mining, which necessitates water-intensive concentration processes.39

Chilean regulations are forcing a transition from continental water to seawater. By 2034, 66% of the water used in Chilean copper mining will be desalinated or reused seawater.39 While this addresses the physical scarcity, it introduces massive costs. Desalinated water can be up to ten times more expensive than groundwater, and pumping water from coastal plants to high-altitude mines (above 2,000 meters) is energy-intensive, with energy accounting for 70% of pipeline operating costs.18

Regional Supply Risks: Geopolitics and Social Unrest

The concentration of copper supply in politically sensitive regions creates a high-risk architecture for global buyers.19

The Democratic Republic of Congo (DRC)

The DRC has become a top-tier producer, with output approaching 3 million tonnes annually.19 However, the DRC is a “strategic bottleneck” where geological wealth is juxtaposed with operational fragility.19 Chronic infrastructure deficits, a “predatory” tax system, and insecurity in eastern provinces create a structural risk environment.19 Kinshasa has moved away from passive rent collection toward assertive “strategic resource sovereignty,” using export quotas and contract renegotiations as leverage.19 For example, in February 2026, the DRC replaced its cobalt export ban with a quota system, capping exports at 96,600 tonnes—a 50% cut from 2024 levels—which significantly tightened associated copper markets.42

Peru and Informal Mining

Peru, the world’s second or third-largest producer, faces recurring labor strikes and social protests that block the “southern mining corridor”.17 In mid-2025, protests by informal miners blocked transit routes for the Las Bambas and Constancia mines, preventing concentrate from reaching the coast and causing a 0.2% drop in national GDP.43 Informal mining is a massive crisis; unauthorized extraction at the Sulfobamba deposit alone represents $950 million in lost resources.44 Communities increasingly view their local informal mining operations as more valuable than corporate compensation offers, leading to long-term stalemates.44

The Midstream Bottleneck: China’s Smelting Hegemony

While copper mining is relatively fragmented, processing is highly concentrated. China processed 45% of the world’s copper in 2024 and controls roughly 40% of global smelting capacity.10 Since 2020, China has increased its refining capacity by 83%.10 This concentration makes global pricing and supply vulnerable to Chinese trade policy and environmental regulations.35

In 2025, the market saw plummeting treatment and refining charges (TC/RCs) as a massive expansion of Chinese smelting capacity met a supply crunch of mine concentrate.46 This situation erodes the margins of independent smelters, potentially deterring new investment in non-Chinese processing capacity.46 Although India (Adani’s Kutch Copper) and Indonesia (Freeport’s Manyar smelter) are adding capacity, China is still expected to account for 50% of refined production by 2040.10

Innovation and Mitigation: Nuton and Substitution

Technological breakthroughs and material substitution are the primary levers for mitigating the projected deficit, though both have significant technical limitations.47

Rio Tinto’s Nuton: Unlocking Waste

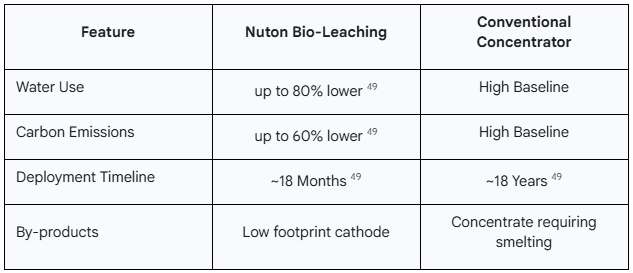

Rio Tinto’s Nuton technology is a bio-heap leaching process that uses microorganisms to extract copper from primary sulfide ores, which were previously too technically challenging or expensive to process.47 This technology can achieve recovery rates of up to 85% from sulfide ore.47

Nuton targets the world’s massive piles of mine waste and low-grade ore, potentially unlocking a “new tonne” of copper without the need for traditional smelters.47 Its first industrial-scale deployment at Arizona’s Johnson Camp mine produced copper with a carbon footprint of 0.82 kg^CO2e/kg, compared to a global average of 3.4 kg.50

Aluminum Substitution: Benefits and Hard Limits

High copper prices (forecast to remain 4.5 times the price of aluminum in 2026) are driving substitution in the automotive and HVAC sectors.51 Aluminum is 30% the weight and 33% the price of copper but only 60-61% as conductive.53

Substituting aluminum for copper in power lines is a mature technology.55 In EVs, aluminum is increasingly used in busbars and wiring harnesses to reduce weight and cost.31 However, there are hard technical limits:

Volume and Space: An aluminum conductor must be 56-60% larger in cross-sectional area to carry the same current as copper, which is often not feasible in compact electronic components or data center racks.57

Battery Chemistry: Aluminum cannot be used as an anode current collector in lithium batteries because it alloys with lithium at low potentials, leading to cell failure.59

Marine and Subsea Environments: Aluminum reacts with water to produce hydrogen gas, which can destroy the insulation of subsea power cables; copper remains the only reliable choice for subsea offshore wind connections.56

Reliability and Creep: Aluminum is prone to “creep” (deformation under stress) and oxidation at connections, requiring regular maintenance that makes it less suitable for high-reliability grid infrastructure.57

Published Forecasts and Outlook for the Supply Deficit

Institutional forecasts generally agree on a structural deficit starting in the mid-2020s, though they vary on the magnitude.

Scenario Analysis: S&P Global and Wood Mackenzie

S&P Global projects that global electricity demand will increase by 50% by 2040, requiring the equivalent of 330 “Hoover Dams” of new capacity.35 This demand will push copper requirements to 42 million metric tons by 2040.2 Without significant investment, primary supply could produce only 22 million metric tons by that date—1 million tons less than today’s levels.35

Wood Mackenzie forecasts that the industry will need 8 million tonnes per annum (Mtpa) of new mine capacity and 3.5 Mtpa of additional scrap by 2035.4 They estimate the total capital requirement to deliver this growth at over $210 billion.20

Near-Term Price Forecasts

Investment banks have significantly raised their price targets for 2026, citing the projected structural deficit.

While some analysts, like those at Goldman Sachs, expect a brief surplus in late 2025/early 2026 due to a “tariff-related correction,” they maintain a bullish long-term outlook, projecting demand to overtake supply permanently from 2029 onwards.51

The Tier-One Project Pipeline: A Reality Check

Meeting the deficit requires the successful development of several massive “Tier-One” projects. However, each faces unique hurdles.

Reko Diq (Pakistan)

The Reko Diq project in Balochistan is one of the world’s largest undeveloped deposits, with a life of 40+ years.63

Phase 1 (2028): Target production of 240,000 t/y copper.64

Phase 2 (2034): Expansion to 460,000 t/y copper.64

Hurdle: The project requires $8.83 billion in total capital, with Phase 1 dependent on securing $3 billion in limited-recourse project financing.64 Operating in Balochistan—Pakistan’s least developed province—introduces significant security and logistical risk.63

Kamoa-Kakula (DRC)

Owned by Ivanhoe Mines, this complex is targeting a return to 550,000 tonnes of annual production.66

Status: Advanced underground rehabilitation is underway following 2025 flooding disruptions.29

Hurdle: The project relies on the Heshima Hydropower Project to ensure reliable energy supply in a region with chronic power deficits.11

Oyu Tolgoi (Mongolia)

Rio Tinto has raised its 2025-2026 forecasts as the underground expansion ramps up.67

Status: Consolidated copper production is expected to reach 860,000-875,000 tonnes by 2025.67

Hurdle: Rio Tinto’s goal is to hit 1 million tonnes per year by 2030, but this requires strict capital discipline and navigating the complexities of Mongolian state partnership.67

Synthesis and Conclusion: The “Powder Keg” Market

The convergence of electrification, AI infrastructure expansion, defense spending, and Asian industrialization has created a “powder keg” in the copper market.5 The evidence indicates that copper is no longer a standard industrial metal but has become the fundamental “strategic bottleneck” of the 21st-century economy.4

Summary of Outlook

Persistent Structural Deficit: Every credible published forecast from S&P Global to Wood Mackenzie indicates a widening shortfall.4 The market is projected to shift from a balanced state in 2025 to a massive deficit of 6-10 million tonnes by 2040.28

Inelastic Supply Response: The 17-29 year permitting timeline and declining ore grades mean that even current record-high prices cannot stimulate immediate supply.10 The “project requirement” for new mines is now 880 ktpa annually—double the rate achieved over the last decade.20

Strategic Geopolitics: Supply concentration in the DRC, Chile, and Peru, combined with China’s 45% share of refining, creates a vulnerable supply chain.10 Policy initiatives like “Project Vault” and the DRC’s export quotas signal that copper is being metabolized by national security interests.26

Technological Limits: While bioleaching (Nuton) and aluminum substitution provide some relief, they cannot bridge a 10-million-tonne gap.47 Substitution is fundamentally limited by the chemical requirements of battery anodes and the volume constraints of digital hardware.57

The “Essentially Infinite Demand” thesis proposed by Robert Friedland is supported by the data on AI power intensity and the mineral-intensive nature of the energy transition.5 For market participants, this points toward a regime of structurally elevated costs and intermittent volatility. The world needs a “generational challenge” level of mining investment, but current financial, regulatory, and geological hurdles suggest that the structural deficit will be a defining feature of the global economy for the foreseeable future.5

Companies of Interest

Exploration & Development (Junior/Mid-Tier)

American Copper Development Corp (ACDC): A Canadian-based explorer focused on the Lordsburg Project in New Mexico. They are targeting large-scale porphyry copper-gold systems and recently transitioned leadership to refocus their strategic goals.

Arizona Sonoran Copper Company (ASCU): Their flagship asset is the Cactus Project (a former ASARCO mine) in Arizona. They are advancing toward becoming a mid-tier producer, with a focus on heap leach operations and on-site copper cathode production.

BeMetals Corp: A diversified explorer with a significant copper footprint in Zambia (the Pangeni Project) and gold projects in Japan. They are backed by industry veterans from B2Gold.

Coppernico Metals Inc: Focused on the Sombrero Project in Peru, which covers a massive land package. They are exploring for copper-gold skarn and porphyry deposits in the same geological belt that hosts world-class mines like Las Bambas.

Copper Giant Resources: Formerly known as Libero Copper & Gold, this company focuses on the Mocoa porphyry copper-molybdenum deposit in Colombia, one of the largest undeveloped copper resources in the region.

Cygnus Metals Ltd: An ASX-listed company revitalizing the historic Chibougamau copper-gold district in Quebec. They aim to use a “hub-and-spoke” model to feed a centralized processing facility from multiple local deposits.

Erdene Resource Development Corp: A Mongolia-focused producer that recently achieved its first gold pour at the Bayan Khundii mine. In the copper space, they are advancing the Zuun Mod project—one of Asia’s largest undeveloped molybdenum-copper deposits—and recently reported high-grade copper intercepts at the nearby Khuvyn Khar porphyry target.

Highland Copper Co: Developing the Copperwood Project in Michigan’s Upper Peninsula. It is one of the few fully permitted copper projects in the U.S., designed as an underground mine with a focus on domestic supply chains.

Kincora Copper Ltd: Active in the Macquarie Arc of New South Wales, Australia. They are exploring for Tier-1 porphyry copper-gold deposits, specifically at their Trundle and Condobolin projects, adjacent to major mines like Northparkes.

Midnight Sun Mining Corp: Focused on the Solwezi Project in Zambia, located directly adjacent to First Quantum’s massive Kansanshi mine. They are targeting high-grade oxide and sulfide copper deposits.

Osisko Metals Inc: Best known for the redevelopment of the Gaspé Copper mine in Quebec. They aim to restart production at this historic site by the early 2030s to meet green energy demands.

Solaris Resources Inc: Their primary asset is the Warintza Project in Ecuador. It is a high-grade, large-scale porphyry copper-gold discovery that has seen significant recent investment for rapid expansion.

XXIX Metals Corp (29Metals): An Australian copper producer (ASX: 29M) with operating mines like Golden Grove and Capricorn Copper. They focus on high-grade copper production with significant precious metal by-products.

Major Global Producer

Teck Resources Ltd: A Canadian mining giant and one of the world’s largest copper producers. Following the sale of its steelmaking coal business, Teck is now a “pure-play” energy transition metals company, highlighted by its massive Quebrada Blanca 2 (QB2) operation in Chile.

FAQs

Why is copper demand rising so fast?

Copper demand is accelerating because modern economic growth is becoming more electric, digital, and infrastructure-intensive. Electric vehicles, renewable energy, power grids, data centers, and defense systems all require far more copper than legacy industrial systems.

An EV uses up to four times more copper than a gasoline car. Solar and wind farms require several times more copper per megawatt than coal plants. AI data centers operate at extreme power densities and need massive wiring and cooling networks. At the same time, emerging economies in India and Southeast Asia are urbanizing and electrifying.

These trends are structural, not cyclical. Once grids, EV fleets, and data centers are built, they lock in long-term copper demand for decades.

How much copper do EVs and charging networks require?

A battery electric vehicle typically contains 60 to 100 kilograms of copper, compared with about 20 kilograms in a conventional car. This includes wiring, motors, inverters, and battery systems.

Charging infrastructure adds another major layer. A single fast-charging station can use several hundred kilograms of copper in cables, transformers, and grid connections. Large highway charging hubs and fleet depots can require several tonnes.

When grid upgrades and transmission lines are included, EV ecosystems can require two to three times more copper than the vehicles alone. By the mid-2030s, EVs and charging networks are expected to consume more than four million tonnes of copper per year globally.

Why do new copper mines take so long to build?

Modern copper mines face three major bottlenecks: permitting, complexity, and capital.

First, environmental reviews, community consultations, and legal challenges can take a decade or more. In the United States and Canada, the process often exceeds 25 years from discovery to production.

Second, new deposits are deeper, lower-grade, and more technically difficult than past mines. They require large-scale processing plants, tailings facilities, water systems, and power infrastructure.

Third, these projects cost billions of dollars and require long-term financing in politically stable environments. Investors demand high confidence before committing capital.

As a result, even mines approved today will not meaningfully increase supply until the 2030s or 2040s.

Can recycling close the copper supply gap?

Recycling helps, but it cannot close the gap on its own.

Globally, recycled copper supplies about 30 to 35 percent of demand. While this share will grow, most copper is locked into long-lived assets such as buildings, power grids, vehicles, and industrial equipment for 30 to 70 years.

Much of today’s copper will not be available for recycling until decades from now. At the same time, electrification is rapidly expanding the installed base.

Even under optimistic scenarios, recycling is expected to cover only a fraction of future demand growth. New primary mines remain essential.

Can aluminum replace copper in grids and data centers?

Aluminum can substitute for copper in some applications, but only partially.

Aluminum is cheaper and lighter, but it is about 40 percent less conductive. To carry the same current, aluminum cables must be much thicker, which creates space, cooling, and safety problems.

In power transmission lines, aluminum already dominates. However, in dense environments such as data centers, EV systems, substations, and electronics, copper remains superior.

Aluminum also suffers from oxidation, mechanical creep, and reliability issues at connection points. In high-reliability systems, these risks are unacceptable.

As a result, substitution can slow demand growth at the margins but cannot eliminate copper’s strategic role.

Why does China’s smelting capacity matter?

China controls roughly 40 to 45 percent of global copper refining and smelting capacity. While mining is geographically diversified, processing is highly concentrated.

Most copper ore must be shipped to China for conversion into refined metal. This gives China significant influence over pricing, treatment charges, and physical availability.

When concentrate supplies tighten, Chinese smelters compete aggressively, driving down processing margins and discouraging new capacity elsewhere. When policy or environmental rules change, global markets feel the impact immediately.

This concentration creates a strategic vulnerability for Western economies and reinforces copper’s role as a geopolitical asset.

What’s the most likely deficit window—late 2020s or early 2030s?

The most acute deficit window is likely from the late 2020s through the mid-2030s.

By 2027–2029, EV adoption, renewable buildouts, and data center expansion are expected to accelerate sharply. At the same time, few major new mines will be coming online.

The early 2030s appear especially vulnerable because demand continues rising while projects approved in the 2020s are still ramping up. Many forecasts show the largest supply gaps between 2030 and 2035.

Without a surge in permitting and investment, the market is likely to experience repeated shortages and price spikes throughout this period.

Works cited

Copper Shortage: Permitting Delays Drive Global Crisis - Discovery Alert, accessed February 5, 2026, https://discoveryalert.com.au/coppers-critical-role-global-economic-framework-2026/

S&P Global: Copper Becoming One of the World’s Most Strategic Commodities | INN, accessed February 5, 2026, https://investingnews.com/sp-global-coppers-strategic-value/

Glencore Copper Production Falls 11% in 2025, accessed February 5, 2026, https://discoveryalert.com.au/copper-market-dynamics-2026-production-volatility/

soaring copper demand an obstacle to future growth | Wood Mackenzie, accessed February 5, 2026, https://www.woodmac.com/press-releases/soaring-copper-demand-an-obstacle-to-future-growth/

Robert Friedland says global economy faces copper crisis - MINING.COM, accessed February 5, 2026, https://www.mining.com/friedlands-copper-crisis-forecast-proves-true-as-historic-supply-crunch-nears/

Analyzing the Key Drivers of the Copper Market in 2025 - MiningNewsWire, accessed February 5, 2026, https://www.miningnewswire.com/analyzing-the-key-drivers-of-the-copper-market-in-2025/

Copper Price Forecast – Market Outlook & Future Trends | Capital.com, accessed February 5, 2026, https://capital.com/en-int/analysis/copper-price-forecast

Forget Energy - Copper Is AI’s Real Bottleneck. Here Are the 2 Miners to Profit Most., accessed February 5, 2026, https://247wallst.com/investing/2026/02/02/forget-energy-copper-is-ais-real-bottleneck-here-are-the-2-miners-to-profit-most/

Copper Market Outlook | J.P. Morgan Global Research, accessed February 5, 2026, https://www.jpmorgan.com/insights/global-research/commodities/copper-outlook

Red Metal Fired Up: The Outlook for Copper - OpenMarkets - CME Group, accessed February 5, 2026, https://www.cmegroup.com/openmarkets/metals/2025/Red-Metal-Fired-Up-The-Outlook-for-Copper.html

Global copper output to grow modestly in 2025, amid supply challenges in Australia and Indonesia - Mining Technology, accessed February 5, 2026, https://www.mining-technology.com/analyst-comment/global-copper-output-grow-modestly-2025/

Structural copper deficit: the thesis that the market is beginning to incorporate | Fynsa, accessed February 5, 2026, https://www.fynsa.com/en/newsletter/deficit-estructural-de-cobre-la-tesis-que-el-mercado-empieza-a-incorporar/

Global Demand for Copper Surges 50% by 2040 - Discovery Alert, accessed February 5, 2026, https://discoveryalert.com.au/copper-essential-role-modern-economies-2026/

Copper prices in 2024 and 2025: a global overview and analysis - Fastmarkets, accessed February 5, 2026, https://www.fastmarkets.com/insights/copper-prices-in-2024-and-2025-a-global-overview-and-analysis/

Indonesian Copper Outlook - Petromindo, accessed February 5, 2026, https://www.petromindo.com/storage/files/research/Indonesian_Copper_Outlookvf.pdf

High prices and by-product gains increasing copper miner margins - Benchmark Source, accessed February 5, 2026, https://source.benchmarkminerals.com/article/high-metal-prices-and-by-product-gains-increasing-copper-miners-margins

Supply Chain Challenges In Copper Mining Industry 2025 - Farmonaut, accessed February 5, 2026, https://farmonaut.com/mining/supply-chain-challenges-in-copper-mining-industry-2025

Why Chile’s mines are turning to the sea, accessed February 5, 2026, https://www.mining-technology.com/features/why-chiles-mines-are-turning-to-the-sea/

DRC: Strategic Minerals, Political Hardening, and the High-Risk Architecture of Global Resource Competition | African Security Analysis, accessed February 5, 2026, https://www.africansecurityanalysis.com/reports/drc-strategic-minerals-political-hardening-and-the-high-risk-architecture-of-global-resource-competition

High-wire act: is soaring copper demand an obstacle to future ..., accessed February 5, 2026, https://www.woodmac.com/horizons/soaring-copper-demand-obstacle-to-future-growth/

Can copper supply keep up with surging demand? | Wood Mackenzie, accessed February 5, 2026, https://www.woodmac.com/blogs/the-edge/can-copper-supply-keep-up-with-surging-demand/

Rio Tinto Glencore Failed Merger: Why Deal Collapsed, accessed February 5, 2026, https://discoveryalert.com.au/rio-tinto-glencore-failed-merger-2026-impact/

Robert Friedland: No Rational Price for Copper as “Essentially Infinite” Demand Meets Short Supply - VVC Resources, accessed February 5, 2026, https://www.vvcresources.com/robert-friedland-no-rational-price-for-copper-as-essentially-infinite-demand-meets-short-supply

accessed February 5, 2026, https://www.nmlegis.gov/handouts/REOTF%20091922%20Item%202%20%20The%20Future%20of%20Copper%20Executive%20Report.pdf

The Future of Copper - S&P Global, accessed February 5, 2026, https://cdn.ihsmarkit.com/www/pdf/0722/The-Future-of-Copper_Full-Report_14July2022.pdf

Ivanhoe Mines Founder and Executive Co-Chairman Robert Friedland Meets with U.S. President Donald J. Trump at the White House for the Launch of Project Vault, a $12 Billion Strategic Critical Minerals Stockpile | TSX:IVN | Press Release - Stockhouse, accessed February 5, 2026, https://stockhouse.com/news/press-releases/2026/02/03/ivanhoe-mines-founder-and-executive-co-chairman-robert-friedland-meets-with-u-s

ESG Economist - Copper is most essential in energy transition | ABN AMRO, accessed February 5, 2026, https://www.abnamro.com/research/en/our-research/esg-economist-copper-remains-very-essential-in-energy-transition

New constraints in the global copper market - The International Institute for Strategic Studies, accessed February 5, 2026, https://www.iiss.org/publications/strategic-comments/2026/new-constraints-in-the-global-copper-market/

Copper Price Disruptions: Mining Risks & Market Impact - Discovery Alert, accessed February 5, 2026, https://discoveryalert.com.au/copper-price-disruptions-supply-chain-2026/

Copper - When Structural Trends Meet Physical Constraints, accessed February 5, 2026,

Visualizing the decline of copper usage in EVs - MINING.COM, accessed February 5, 2026, https://www.mining.com/web/visualizing-the-decline-of-copper-usage-in-evs/

Copper Demand from Data Centers: AI Infrastructure Growth - Discovery Alert, accessed February 5, 2026, https://discoveryalert.com.au/electrical-infrastructure-requirements-data-center-2026/

Copper Rally Accelerates as AI Data Centers Push Supply Toward Crisis Levels, accessed February 5, 2026, https://www.investing.com/analysis/copper-rally-accelerates-as-ai-data-centers-push-supply-toward-crisis-levels-200671454

The copper supply shortage threatens AI data centers and the global electrification effort... | Yellow Media French on Binance Square, accessed February 5, 2026, https://www.binance.com/en/square/post/35560028466458

‘Substantial Shortfall’ in Copper Supply Widens as the Race for AI and Growing Defense Spending Add to Accelerating Demand, New S&P Global Study Finds - PR Newswire, accessed February 5, 2026, https://www.prnewswire.com/news-releases/substantial-shortfall-in-copper-supply-widens-as-the-race-for-ai-and-growing-defense-spending-add-to-accelerating-demand-new-sp-global-study-finds-302656062.html

Mine development times: The US in perspective - S&P Global, accessed February 5, 2026, https://cdn.ihsmarkit.com/www/pdf/0724/SPGlobal_NMA_DevelopmentTimesUSinPerspective_June_2024.pdf

Leading the World in Resources, Trailing the Competition in Access - National Mining Association, accessed February 5, 2026, https://nma.org/resources/fact-sheet-leading-the-world-in-resources-trailing-the-competition-in-access/

Projected Copper Shortfall: Supply Crisis Investment Guide - Discovery Alert, accessed February 5, 2026, https://discoveryalert.com.au/copper-supply-demand-imbalance-2026-investment-analysis/

From Freshwater to Seawater: Water Demand in Chilean Copper Mining Outlook - ax | legal, accessed February 5, 2026, https://ax.legal/2025/06/17/from-freshwater-to-seawater-water-demand-in-chilean-copper-mining-outlook/

2025 Democratic Republic of the Congo (DRC) Investment Climate Statement - State Department, accessed February 5, 2026, https://www.state.gov/wp-content/uploads/2025/09/638719_2025-Democratic-Republic-of-the-Congo-Investment-Climate-Statement.pdf

Full Year 2025 Production Report - Glencore, accessed February 5, 2026, https://www.glencore.com/media-and-insights/news/full-year-2025-production-report

Copper’s next shortage is structural, not hype: analyst - The Northern Miner, accessed February 5, 2026, https://www.northernminer.com/news/coppers-next-shortage-is-structural-not-hype-analyst/1003885764/

MMG and Hudbay warn of impact from informal miners’ protests in Peru - Mining Technology, accessed February 5, 2026, https://www.mining-technology.com/news/mmg-hudbay-minerals-copper-mine-peru/

Illegal Copper Mining Peru: $950M Crisis Exposed - Discovery Alert, accessed February 5, 2026, https://discoveryalert.com.au/illegal-copper-mining-peru-2025-impacts-crisis/

‘Substantial Shortfall’ in Copper Supply Widens as the Race for AI and Growing Defense Spending Add to Accelerating Demand, New S&P Global Study Finds - Jan 8, 2026 - Press Releases, accessed February 5, 2026, https://press.spglobal.com/2026-01-08-Substantial-Shortfall-in-Copper-Supply-Widens-as-the-Race-for-AI-and-Growing-Defense-Spending-Add-to-Accelerating-Demand,-New-S-P-Global-Study-Finds

The India Copper Report - CSEP, accessed February 5, 2026, https://csep.org/wp-content/uploads/2025/08/The-India-Copper-Report.pdf

Nuton: A faster, cleaner way to produce copper | Global - Rio Tinto, accessed February 5, 2026, https://www.riotinto.com/en/news/stories/nuton-a-better-way-to-produce-copper

Is Aluminum the Next Copper? - Addionics, accessed February 5, 2026, https://addionics.com/blog/is-aluminum-the-next-copper/

Rio Tinto Supplies New Breakthrough Low-Carbon Copper for Amazon Data Centers, accessed February 5, 2026, https://www.esgtoday.com/rio-tinto-supplies-new-breakthrough-low-carbon-copper-for-amazon-data-centers/

Rio Tinto’s Nuton technology produces first copper | Global, accessed February 5, 2026, https://www.riotinto.com/en/news/releases/2025/rio-tintos-nuton-technology-produces-first-copper

Copper Prices Are Forecast to Decline Somewhat from Record Highs in 2026, accessed February 5, 2026, https://www.goldmansachs.com/insights/articles/copper-prices-forecast-to-decline-from-record-highs-in-2026

A strategic choice: Changing from copper to aluminium in HVAC&R and automotive applications | Hydro, accessed February 5, 2026, https://www.hydro.com/en/global/about-hydro/stories-by-hydro/a-strategic-choice-changing-from-copper-to-aluminium-in-hvacr-and-automotive-applications/

Cooking Up a Conductive Alternative to Copper with Aluminum | Feature | PNNL, accessed February 5, 2026, https://www.pnnl.gov/news-media/cooking-conductive-alternative-copper-aluminum

Copper VS Aluminum: Using Aluminum to Replace Copper in the Power Sector, accessed February 5, 2026, https://www.jingdawire.com/blogs/copper-vs-aluminum-guide/

How we can substitute aluminium for copper in the green transition - Shapes by Hydro, accessed February 5, 2026, https://www.shapesbyhydro.com/en/material-properties/how-we-can-substitute-aluminium-for-copper-in-the-green-transition/

Copper vs. Aluminum: Choosing Wind Farm Cabling - KLZ Cables, accessed February 5, 2026, https://klz-cables.com/cost-comparison-copper-vs-aluminum-cables-in-wind-farms-which-is-worthwhile-in-the-long-term/

Why use copper rather than aluminium as the conductor in power cables?, accessed February 5, 2026, https://help.leonardo-energy.org/hc/en-us/articles/205394842-Why-use-copper-rather-than-aluminium-as-the-conductor-in-power-cables

Aluminum cables or copper cables? - Prysmian, accessed February 5, 2026, https://tr.prysmian.com/en/media/technical-article/aluminum-cables-or-copper-cables

Global Copper Crisis: Do We Have Alternatives? - IMDEA Materials, accessed February 5, 2026, https://materials.imdea.org/global-copper-crisis-do-we-have-alternatives/

Powerful Thinking: Aluminium vs Copper: The Battle of Cable Core in Power Systems, accessed February 5, 2026, https://visionsustainableevents.org/powerful-thinking-aluminium-vs-copper-the-battle-of-cable-core-in-power-systems/

Analysis: copper set for new investment, recycling growth, accessed February 5, 2026, https://resource-recycling.com/e-scrap/2025/10/23/analysis-copper-set-for-new-investment-recycling-growth/

Why Record-High Copper Prices Aren’t Forecast to Last | Goldman Sachs, accessed February 5, 2026, https://www.goldmansachs.com/insights/articles/why-record-high-copper-prices-arent-forecast-to-last

ADB Approves Financing for Transformative Reko Diq Copper Mining Project in Pakistan, accessed February 5, 2026, https://www.adb.org/news/adb-approves-financing-transformative-reko-diq-copper-mining-project-pakistan

Reko Diq copper/gold project, Pakistan – update - Mining Weekly, accessed February 5, 2026, https://newsletter.mw.creamermedia.com/article/reko-diq-coppergold-project-pakistan-update-2025-04-11

Fluor Receives Final Notice to Proceed from Barrick on Reko Diq Copper Project in Pakistan, accessed February 5, 2026, https://newsroom.fluor.com/news-releases/news-details/2025/Fluor-Receives-Final-Notice-to-Proceed-from-Barrick-on-Reko-Diq-Copper-Project-in-Pakistan/default.aspx

Ivanhoe Mines Announces Kamoa-Kakula Copper Production Guidance for 2026 and 2027 as Recovery Plan Advances, accessed February 5, 2026, https://www.ivanhoemines.com/news-stories/news-release/ivanhoe-mines-announces-kamoa-kakula-copper-production-guidance-for-2026-and-2027-as-recovery-plan-advances/

Rio Tinto Revises Up 2025 Copper Production Forecast as Mongolian Project Accelerates Operations. - Shanghai Metals Market (SMM), accessed February 5, 2026, https://news.metal.com/newscontent/103655485-Rio-Tinto-Revises-Up-2025-Copper-Production-Forecast-as-Mongolian-Project-Accelerates-Operations