Minaurum Silver Inc.

An emerging project with potentially 30 million ounces of silver

Company Overview and Project History

Minaurum Silver Inc is a Canadian precious metals exploration company listed on the TSX Venture Exchange (TSXV: MGG) and OTCQX (MMRGF). The company is focused on the discovery and advancement of high-grade silver and gold projects in Mexico. Minaurum’s strategy emphasizes district-scale exploration in historically productive mining regions, targeting epithermal vein systems with the potential for underground, high-margin development scenarios.

The company’s flagship asset is the Alamos Silver Project, a 100% owned property located in southern Sonora, Mexico, approximately 8 km west of the city of Alamos. The project comprises roughly 37,900 hectares and benefits from excellent infrastructure, including paved road access, available power, water, and proximity to an experienced regional mining workforce. Importantly, the central project area has an approved Environmental Impact Statement (MIA) that permits surface exploration and underground mine development activities, including the rehabilitation of historical workings.

Alamos is a low-sulphidation epithermal vein system hosted within a structurally controlled district that contains at least 26 identified vein zones. Historic mining occurred intermittently from the late 1800s through the mid-20th century, primarily exploiting high-grade silver mineralization from shallow underground workings. Modern systematic exploration by Minaurum began in the mid-2010s and included surface mapping, geophysics, and diamond drilling.

Between 2016 and 2025, Minaurum completed multiple drilling campaigns, progressively defining mineralization along the Promontorio, Travesía, and Europa vein zones. Drilling demonstrated consistent high grades over mineable widths, including numerous multi-meter intervals exceeding 200 g/t silver equivalent, with localized bonanza-grade shoots.

On January 28, 2026, Minaurum announced its initial NI 43-101 compliant Inferred Mineral Resource Estimate for Alamos. The resource totals 5.37 million tonnes grading 202 g/t silver, 0.21 g/t gold, 0.43% copper, 0.97% lead, and 2.01% zinc (320 g/t silver equivalent), containing 34.8 million ounces of silver and 55.2 million ounces silver equivalent. The estimate is based on 104 drill holes totaling approximately 35,900 meters and is reported at a 150 g/t silver equivalent cut-off grade.

The current resource encompasses only three of the 26 known vein zones, and mineralization remains open along strike and at depth. A 50,000-meter Phase II drill program is underway to expand and upgrade the resource base, with the objective of supporting future economic studies.

Given its high grade, established underground access, district-scale potential, and existing permits allowing development activities, Alamos represents an advanced exploration asset with characteristics suitable for a high-margin underground mining operation.

Below is a simplified “proto‑PEA” based on Minaurum Silver’s January 2026 NI 43‑101 resource estimate for the Alamos project. It is hypothetical and is not an official economic study. I have used public data for the resource, typical operating costs and mining methods of comparable epithermal vein deposits to illustrate possible economics.

Resource and deposit context

Resource: Minaurum’s January 28 2026 news release reports an inferred resource of 5.37 Mt grading 202 g/t Ag, 0.21 g/t Au, 0.43 % Cu, 0.97 % Pb and 2.01 % Zn (320 g/t AgEq). This contains 34.8 M oz silver, 35 640 oz gold, 51.0 M lb copper, 115 M lb lead and 238 M lb zinc. The resource is reported at a 150 g/t AgEq cut‑off with an effective date of 8 Jan 2026; commodity price assumptions are US$29.73/oz Ag, US$2 646/oz Au, US$4.34/lb Cu, US$0.92/lb Pb and US$1.21/lb Zn. The deposit is a low‑sulphidation epithermal vein system in southern Sonora, hosted by multiple steeply dipping veins within a large land package; Minaurum holds 100 % ownership and the site is permitted for exploration and mine construction.

Logical mining process: Epithermal vein deposits such as Alamos are typically mined by underground methods using ramp access, sub‑level stoping and mechanized cut‑and‑fill or long‑hole stoping, with paste or rock fill for backfilling. Comparable Mexican operations like Endeavour Silver’s Terronera project use a ramp‑accessed underground mine with long‑hole drilling and cut‑and‑fill stoping, followed by conventional flotation to recover silver and gold. The Mercedes gold‑silver mine in Sonora also relies on mechanised cut‑and‑fill stopes, with long‑hole open stopes where rock quality allows. These methods suit narrow, steeply dipping veins and minimise dilution. Given the permitting for underground development at Alamos and the block size used in the resource model (5 m × 1 m × 2.5 m), a similar underground mining and flotation process is a logical assumption.

Typical AISC in Mexico: Silver mines in Mexico report a wide range of all‑in sustaining costs (AISC). Endeavour Silver’s 2024 guidance estimates AISC of US$22–23 per oz silver (net of by‑product credits). Americas Gold and Silver’s Q2‑2024 results report AISC of US$19.58 per silver ounce. The Silver Institute’s 2025 World Silver Survey notes that in 2024 the average AISC for primary silver mines in Mexico fell to about US$13.77/oz, driven by higher by‑product revenue and lower sustaining capital. For this proto‑PEA I assume AISC ≈ US$22/oz, which is toward the upper end of this range to reflect potential underground development costs.

Proto‑PEA assumptions and calculations

Recovered silver: Using the inferred resource of 34.8 M oz silver and assuming metallurgical recovery of 82.6 % (based on Terronera’s flotation recoveries), total recovered silver would be ≈28.7 M oz. Dividing this over a 12‑year mine life yields ~2.4 M oz of recovered silver annually.

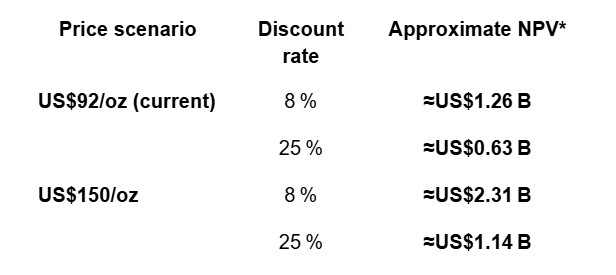

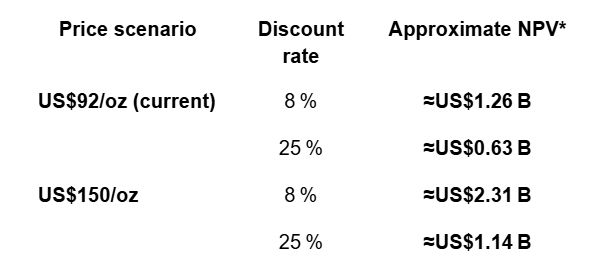

Operating margin: At an assumed AISC of US$22/oz, operating margins per ounce are (silver price – 22). Two price scenarios are examined:

Current price (~US$92/oz): Fortune and Forbes reports show that on 27 Feb 2026 silver traded around US$92 per ounce. The margin is ≈US$70/oz.

Upside price (US$150/oz): This scenario tests a much higher silver price; the margin is US$128/oz.

Cash flows and NPV: Annual cash flow = margin × 2.4 M oz. Assuming constant production and ignoring capital costs, taxes, sustaining capital and revenue from gold/copper/lead/zinc, the net present values (NPV) were calculated at 8 % and 25 % discount rates.

*NPVs are based on recovered silver only (28.7 M oz), AISC of US$22/oz, a 12‑year life and constant annual production; they exclude capital costs, sustaining capital, taxes, inflation and revenues from other metals, so they serve only as rough indicators of leverage to silver prices.

Interpretation

The proto‑PEA suggests that the Alamos resource could generate significant free cash flow at current silver prices if a high‑grade underground mine is developed. At US$92/oz, an 8‑% discount NPV of about US$1.26 B indicates a robust margin even after assuming a relatively high AISC. At higher silver prices, the project’s leverage becomes more pronounced. However, these results are not definitive economic indicators because they omit capital expenditures (capex), sustaining capital, project financing, tax considerations and contributions from gold and base metals. They also assume all inferred resources convert to reserves and are mined at consistent grades, which may not occur. A formal Preliminary Economic Assessment (PEA) would require detailed engineering, metallurgical testing, mine planning and cost estimation to confirm viability.